Dealing with taxes has never been easy, and the nascent cryptocurrency space and its various innovations have only made things harder. As governments struggle to adapt to the nascent space with new regulations, crypto traders struggle to understand how to pay crypto taxes.

While it isn’t easy to understand how much you have to pay in taxes on your own, it’s important to figure things out either way. In the United States, for example, not paying them is considered tax fraud and can lead to a maximum prison sentence of five years, or a $250,000 fine.

In the United States, the Internal Revenue Service (IRS) had revealed the taxpayer has to compile all needed information by itself, meaning they have to go through every single trade and transaction, record the necessary data, and determine whether they’ve made a profit or not.

In most countries, individuals are liable to pay capital gains tax when they sell their cryptoassets, as most governments see cryptos as digital property. Cryptocurrency miners aren’t exempt in most cases, as cryptoassets earning securing blockchain are often subject to income taxes, qualified as self-employment.

Tracking every single trade one has made over the course of a year can seem daunting, and if cryptocurrency traders or investors also mine then dealing with cryptocurrency taxes may be a huge burden. To help there are various tools out there that can automatically fill in transaction data and calculate gains or losses.

CryptoCompare caught up with top crypto tax tools CoinTracking, CoinTracker, ZenLedger, Koinly, Bitwave, CryptoTax, BearTax, and Blockpit to get into common mistakes people make when it’s time to do their crypto taxes, their thoughts on current regulations, exchanges’ role in crypto taxes, and more.

Most Don’t Pay Taxes on Cryptocurrencies

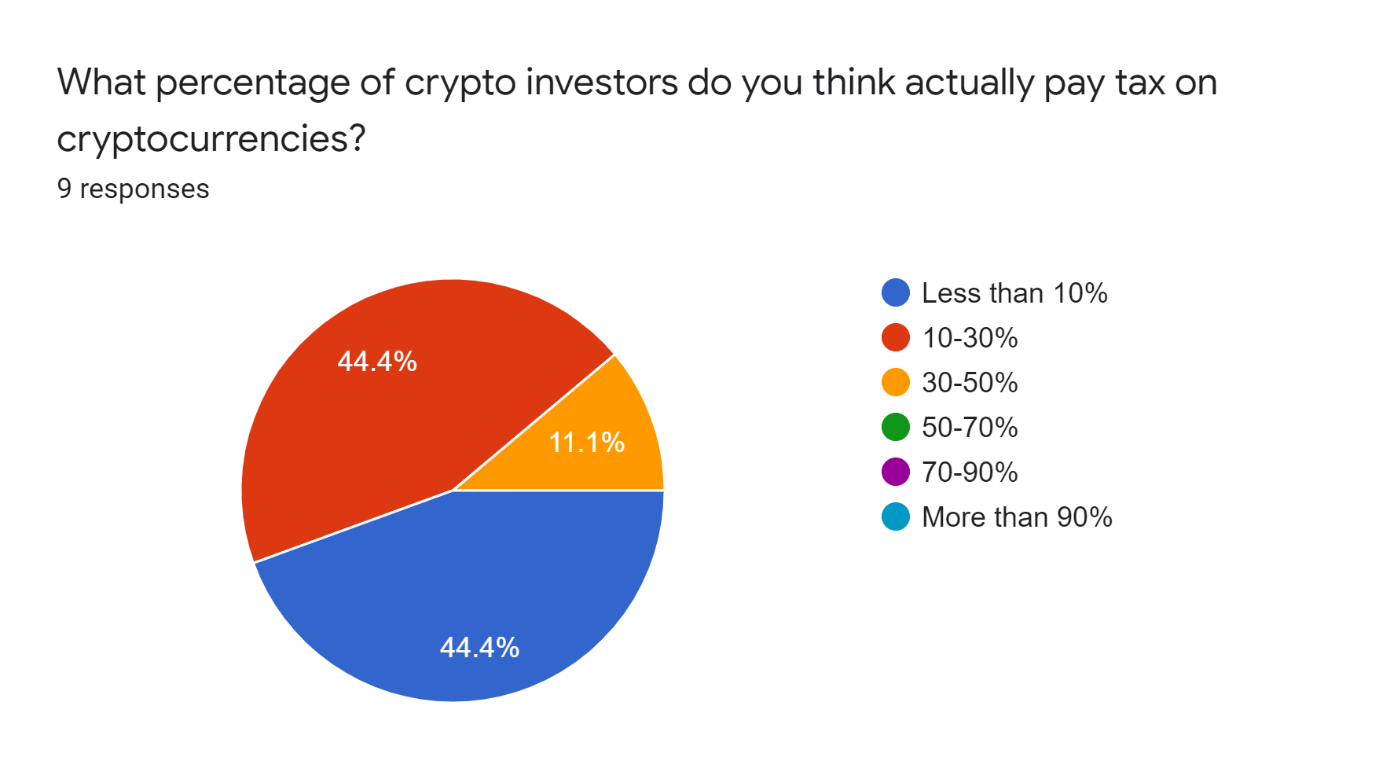

Cryptocurrency tax tool operators have revealed they think most cryptocurrency users do not pay related taxes. In our survey, 44.4% of respondents said they believe less than 10% of crypto users pay taxes on cryptocurrencies, while another 44.4% said the figure is between 10% and 30%. 11.1% said the figure could go as high as 50%.

When asked about how many jurisdictions they support, most tools revealed they had a rather limited range, with the US and UK coming in most of the answer. Others included jurisdictions in Europe, Australia, Canada, and more. Two revealed they provide “generic” reports for other counties.

On top of the lack of support for users in some jurisdictions, cryptocurrency exchanges seemingly aren’t making it easy to pay cryptocurrency taxes. When asked whether they believe exchanges are facilitating things, most pointed towards the negative.

Most cryptocurrency exchanges, they said, are focusing on offering their users proper liquidity and security for now, instead of providing users clear and simple resources to get their taxes done – something one respondent said “would be considered unacceptable in the non-crypto financial world.”

Another respondent said:

"I think we are still far from an ideal situation, but we are getting there. The big issue is, that a single exchange can't give you correct tax reports, as soon as you are involving any other exchange or external wallet there will be missing data, that can't be interpreted."

These complications mean third-party platforms end up being required either way, as these can combine and standardize data from multiple sources. Other respondents agreed, pointing out that while “some exchange have good data export features” others “only let you export part of the data you need to do your taxes.”

The lack of a clear industry standard when it comes to the data needed for cryptocurrency-related taxes and the lack of adequate customer support teams to assist customers during tax season were also flagged.

Taxation Uncertainty

Decentralized exchanges and decentralized finance have made things even harder for those wanting to pay cryptocurrency-related taxes, Respondents revealed that decentralized finance protocols pose “a challenge both from the data and the tax perspective.”

In many cases, another respondent said, there isn’t a company behind the smart contract users interact with to provide them with a tax report. They added:

“This on top of the unique types of transactions that don't exist outside of cryptocurrency introduce unique situations that false outside of tax precedent. They are also often harder to track given the integrations required with smart contracts and on-chain data.”

Others point out that data aggregation can be a problem, and that non-user-friendly transaction history will make it harder for tax tools to import data. In many scenarios, there are “lots of gray areas, where a lot of research has to happen.” Until then, they will be left for the interpretation of accountants.

Another respondent summed the situation up by pointing out that “DeFi tax requirements are still unclear.” The lack of guidance from the IRS on the nascent space leaves room for interpretation.

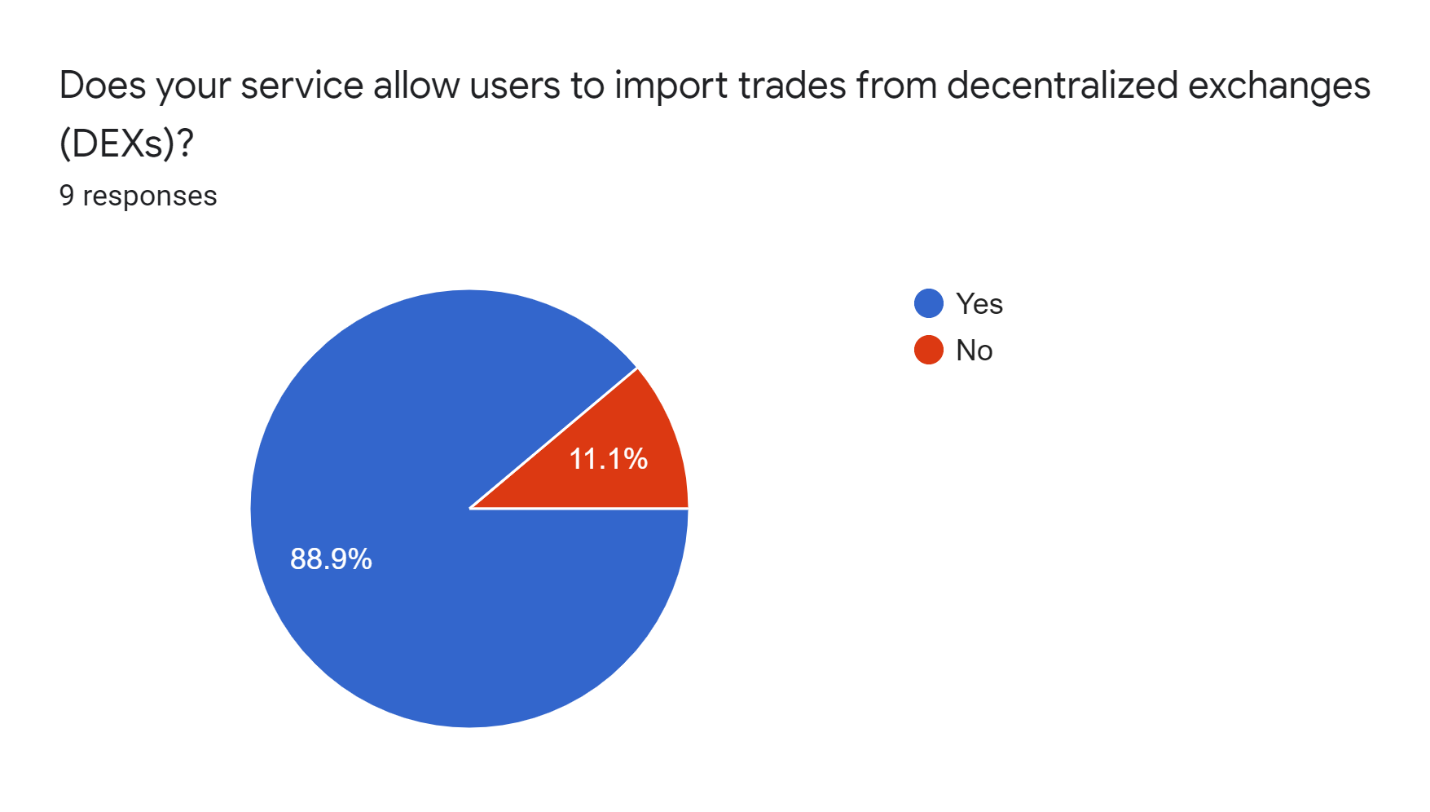

Those using decentralized trading platforms, which as we have seen are expected to keep on growing in the near future, already have services allowing users to important traders from there.

Innovations like DeFi, however, pose a new challenge and these types of innovations in the cryptocurrency space aren’t new, and are likely going to keep going. From ICOs to airdrops, a lot ends up in a gray area, as regulators fail to react quickly enough to these developments.

When Will We Be Able to Pay Taxes With Crypto?

When asked whether the United Kingdom and the United States introduced sensible laws regarding cryptocurrency taxes, respondents showed mixed feelings. While some pointed out that current frameworks make things clear for users to pay taxes, others pointed out there are a lot of lingering uncertainties.

Respondents agreed regulators “seem to be putting in considerable efforts in drafting the guidance and rules,” but noted that while for most cryptocurrency users things are clear, those interacting with DeFi protocols and other innovations make things harder.

Some of the regulations may, however, be hindering adoption. One respondent said:

“Taxation of small transactions used for regular payments is hindering the adoption as well as general usage. Intention of transacting cryptocurrency should be considered while taxation because someone might be using crypto to buy a guitar vs someone profiting off an arbitrage trade.”

Countries in Europe have reportedly already adopted exemptions for when users convert cryptocurrencies to fiat for small transactions, such as when they are buying coffee. In the U.S., they argued, the best guidance from the IRS was issued in 2014 – six years ago – before ICOs, DeFi, and yield farming.

When asked about a potential time in which we will be using cryptocurrencies to pay for taxes most experts agreed that, in the future, it will be globally accepted. One noted that if “you believe in cryptocurrencies taking off, paying taxes in crypto is inevitable.”

Another respondent said:

“Yes, it would. Most of the US, AU, UK are already considering this as an asset class and trying to provide tax documents as necessary to their accountants. It's only about the pain at the end of the year - which we are trying to address and alleviate.”

It’s worth pointing out that Switzerland’s canton of Zug, home to the so-called “Crypto Valley,” will start accepting bitcoin and ether for tax payments in February 2021. To some crypto tax tool operators, however, this is nothing but a “marketing stunt.”

The top cryptocurrencies with the most liquidity, they argued, are “still very volatile” and as such there isn’t a lot of value in paying taxes in cryptocurrencies. Another respondent claimed that “paying taxes in crypto is not really a solution for anything.”

Top Tips for Filing your Crypto Taxes

CryptoCompare then asked the cryptocurrency tax tool operators about the most common mistakes people make when it comes to doing their crypto taxes. Data input errors, missing data, and relying on tracking tools that aren’t suited for tax reporting were among the top answers.

Other common mistakes included not following official guidance, and failure to keep records in case an exchange shuts down. One respondent pointed out that starting to work on crypto taxes too late is also a common mistake:

“Once you have accumulated a lot of transactions on multiple exchanges, have used many wallets, participated in airdrops, tokensales and the like it gets really cumbersome to "re-create" your trading history from scratch.”

Finally, traders should take into account the accounting method they will be using when filing their taxes, and adapt their trading strategies accordingly to optimize their gains.

Most of these problems can be offset with the use of proper cryptocurrency tax reporting tools. We would like to thank BearTax, CryptoTax, CoinTracker, Bitwave, CoinTracking, Blockpit, Koinly, and ZenLedger for participating in our survey.

Important information

This website is only provided for your general information and is not intended to be relied upon by you in making any investment decisions. You should always combine multiple sources of information and analysis before making an investment and seek independent expert financial advice.

Where we list or describe different products and services, we try to give you the information you need to help you compare them and choose the right product or service for you. We may also have tips and more information to help you compare providers.

Some providers pay us for advertisements or promotions on our website or in emails we may send you. Any commercial agreement we have in place with a provider does not affect how we describe them or their products and services. Sponsored companies are clearly labelled.

Opera

Opera

Internet Explorer

Internet Explorer